The Future of Cross-Border Payments Runs on Stablecoins

Dailycoin

Banks that fail to use stablecoins for cross-border payments risk losing business, facing higher costs, and fading into obscurity.

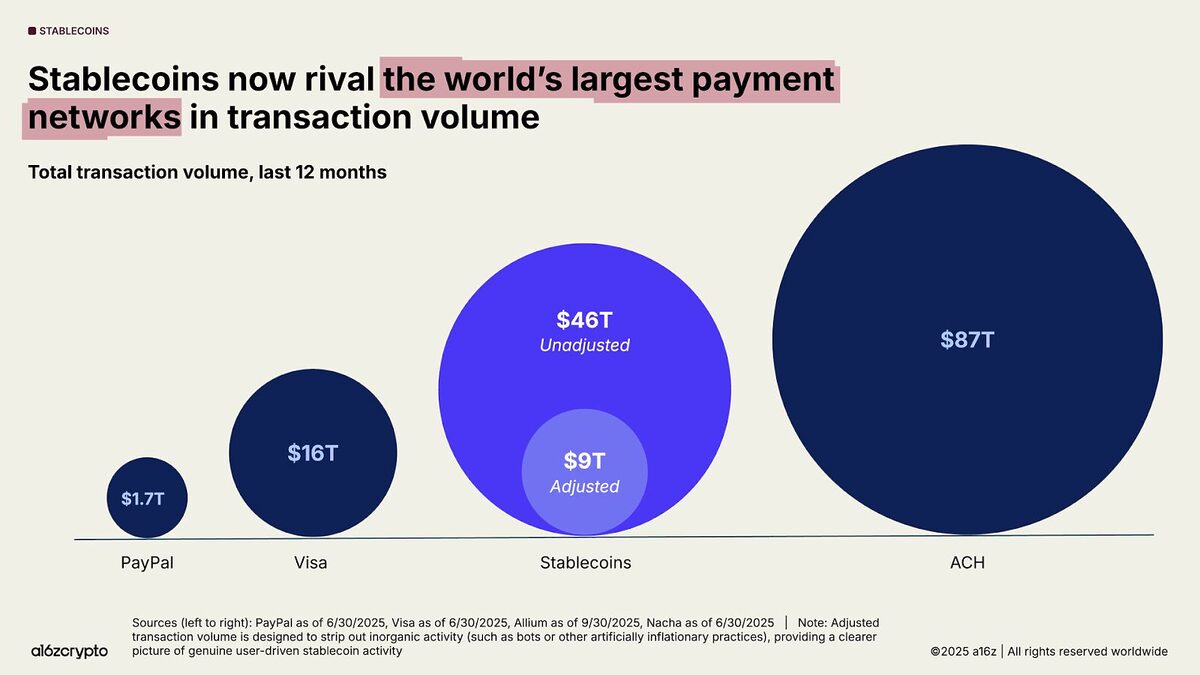

The global cross-border payments system facilitates $150 trillion in annual transactions, a feat that has driven decades of international trade and economic growth.

Stablecoins are on track to replace this system entirely.

The question isn’t whether this will happen; it’s how fast the $150 trillion annual payment volume shifts from legacy banking networks to stablecoins. For reasons unrelated to blockchain hype, it could happen faster than most finance professionals expect.

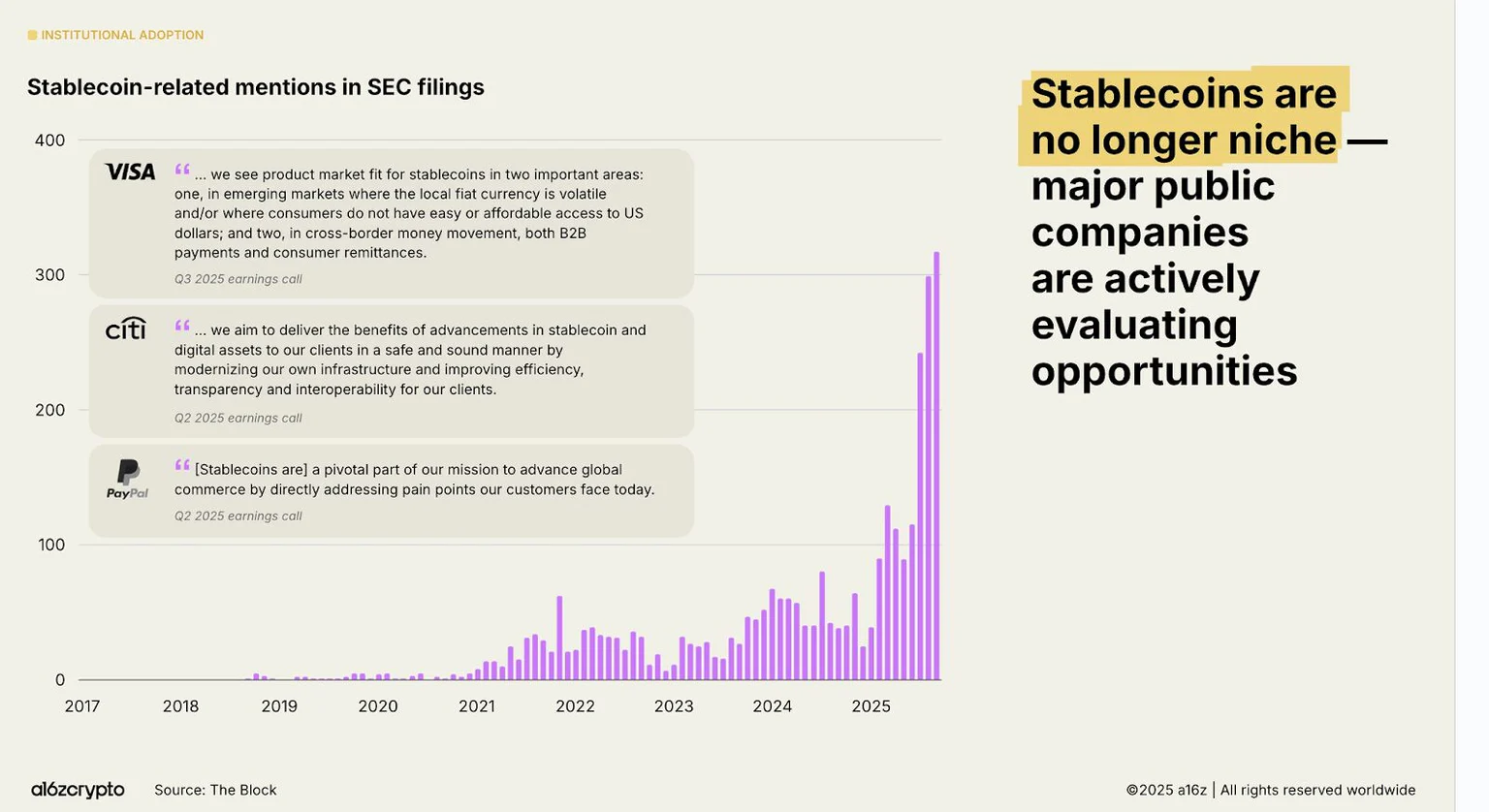

Here’s why: Institutions are racing to replace legacy payment systems with stablecoins. 15% of banks now offer them, and 57% percent are actively exploring adoption.

KPMG’s latest report on stablecoins validates what those of us building in this space already know: the current system is painfully inefficient, and stablecoins can eliminate its structural problems.

The Current System Can’t Compete

If you pitched SWIFT, the decades-old messaging network banks use to move money across borders, as a business model today, you would be laughed out of the meeting.

Today, legacy cross-border payments take 2-5 days to settle, cost $25-$35 per transaction, and require banks to lock up billions in nostro and vostro accounts worldwide.

According to KMPG, stablecoins cut this settlement time to mere seconds and slash costs up to 99%.

Stablecoins will dominate this space, not because they’re the only blockchain solution, but because they’re the only one that solves the problem without creating new dependencies.

Stablecoins vs Ripple & CBDCs

Stablecoins beat CBDCs, and Ripple’s payment solutions like XRP and RippleNet, because while they can improve settlement times and costs, they introduce vendor control and governance trade-offs that institutions try to avoid.

CBDCs centralise power. They allow governments to freeze funds, restrict spending, and enforce capital controls across borders, the opposite of what institutions want in a settlement asset.

The Bank for International Settlements (BIS) warns that CBDCs could create fragmented “digital islands” in cross-border payments as each country builds its own system with different technical standards and compliance rules.

Meanwhile, Ripple’s services concentrates control in one vendor, creating a governance bottleneck. The FSB warns that using volatile crypto-assets like XRP for settlement can expose institutions to significant market and liquidity risk.

Stablecoins avoid these dependencies by operating across multiple chains, custody models, and compliance frameworks. They provide programmable money with predictable value, which counterparties are willing to hold.

Fragmentation Is Temporary in Stablecoin Settlement

The downside to stablecoins is that they’re fragmented across Ethereum, Solana, private networks, and other chains, which has been a challenge for adoption. Today, this is just an intermediate phase.

New middleware is emerging that routes payments across different blockchains in real time, optimizing for cost, liquidity, and compliance. Cross-chain settlement engines can already execute transactions atomically rather than relying on intermediaries.

This multi-chain design offers institutions more flexibility. Banks can select settlement layers that fit regulatory requirements and cost structures, while treasury teams manage liquidity dynamically across networks. If this infrastructure continues to scale, foreign-exchange settlement could move from T+2 to near-instant execution, which would mean a structural shift in cross-border finance.

Will Multiple Blockchain Systems Coexist?

According to BIS, multiple settlement systems will likely coexist in the near term as legacy infrastructure, CBDC pilots, and correspondent banking networks operate alongside stablecoins.

However, as stablecoin networks become more established, with growing liquidity and lower costs, it will become increasingly difficult for older systems to compete. Once today’s trial phase ends, cross-border payments will likely settle on the fastest and cheapest option, and right now, that’s stablecoins.

In October 2025 alone, several major institutions announced partnerships to pilot compliant stablecoin payments, including Western Union’s integration with Solana, Citi’s collaboration with Coinbase, and ClearBank’s work with Circle. These initiatives signal that traditional financial entities are increasingly favouring stablecoins as production infrastructure.

The Outcome Is Predictable

Banks that ignore stablecoin settlement will pay more, lose customers, and struggle to stay relevant as the industry shifts to faster rails. This shift is not ideological; it’s driven by a widening efficiency gap as settlement times collapse from days to seconds and costs fall close to zero. Legacy systems simply cannot compete with that cost curve.

The institutions moving first are not speculators; they are conservative treasury teams responding to balance-sheet logic and liquidity incentives. The October KPMG report confirms that this transition is underway, and momentum is building faster than many incumbents expected.

Stablecoins are on track to overtake SWIFT and proprietary vendor systems as the default settlement layer for cross-border payments. The only question is whether banks adapt early, or find themselves chasing network effects that have already locked in.

About the Author

Howard Davidson is the CMO of Almond FinTech. Almond is building the intelligence layer for global money movement-a programmable FX and treasury orchestration engine optimizing payments across all blockchains and tokens.